Why Oil Prices Are Rising

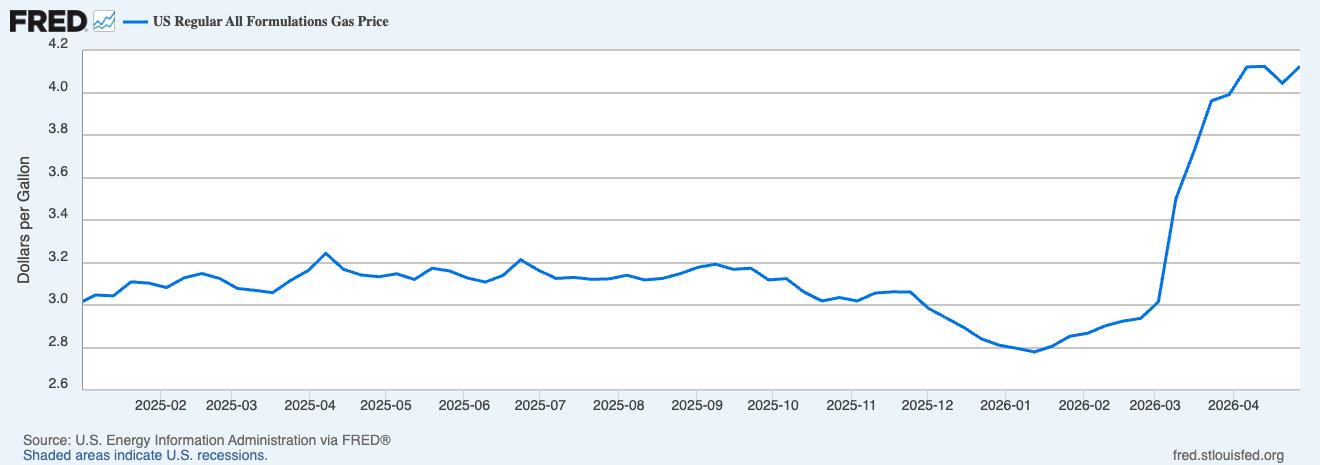

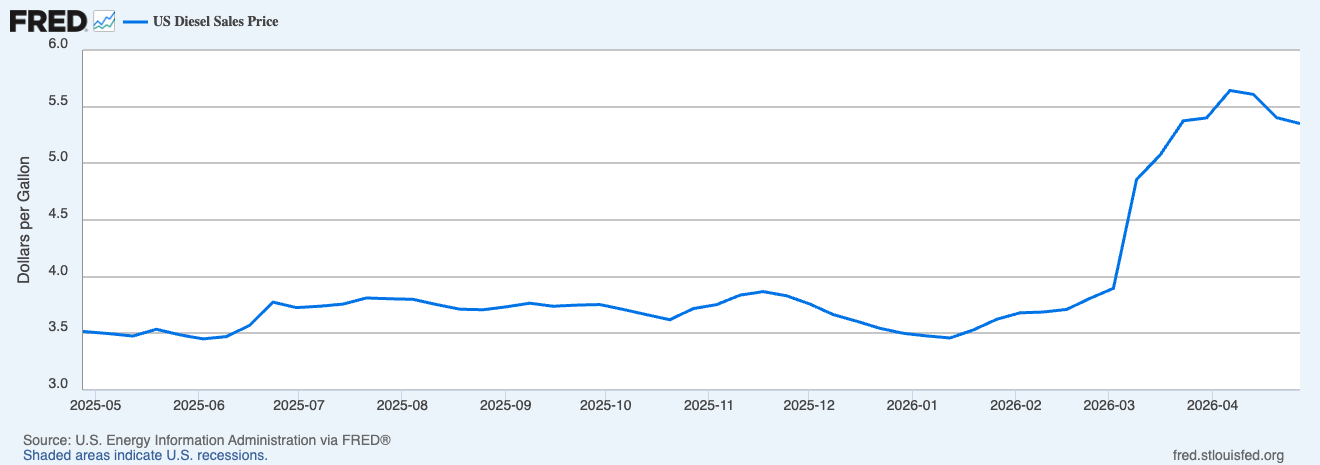

If you’ve driven at all in the past few months, you have probably noticed that oil prices have risen. In fact, oil prices in the U.S. are at their highest levels since 2022. The conflict involving Iran that began in late February led to a sudden and severe disruption of global oil supply, primarily due to the closure of the Strait of Hormuz, the transit route for roughly 20% of the world’s oil.1 As a result, international crude prices skyrocketed. Brent crude oil spiked from around $70 per barrel before the conflict to as high as $118 by the end of March.2 Even after a temporary ceasefire in April brought some relief, Brent remains near $95–$100 (mid-April), reflecting a hefty geopolitical risk premium.3 U.S. gasoline and diesel prices surged as a result, since fuel is priced in a global market, not just the U.S. standard, West Texas Intermediate. By late March, the national average gasoline price broke above $4 per gallon for the first time in over three years — up more than 30% in a month — a jump of roughly $1 per gallon from late February.4 Diesel, the primary fuel for trucks and heavy equipment, climbed even faster: it crossed $5 per gallon by mid-March and is now about 40–45% higher than before the conflict. These prices remain just shy of their all-time highs set in 2022, but the speed of the increase has been unprecedented in decades.5

The Strait of Hormuz Disruption and OPEC Supply Shock

Multiple factors have fed into this rapid rise in fuel prices. Global supply has tightened dramatically. The war effectively removed millions of barrels of oil per day from the market by halting exports from key OPEC producers. In fact, OPEC’s output plunged by about 7.5 million barrels per day in March — a 25% collapse to 22 million barrels per day — as Saudi Arabia, the UAE, and others were forced to curtail production due to shipping blockades.6 This supply shock is the largest since the 1970s energy crises, and according to the International Energy Agency is the biggest oil supply disruption in history. Meanwhile, last month the OPEC+ alliance, a broader coalition of OPEC and non-OPEC oil producers, signaled reduced expectations for near-term oil demand due to the war’s economic fallout. However, any voluntary output cuts or demand downgrades by OPEC+ have been overshadowed by the immediate involuntary shut-in of supply.

Geopolitical Risk, Refinery Constraints, and Seasonal Demand

Geopolitical risk and seasonality have amplified the price volatility. Fears of further escalation — including threats to oil infrastructure — led to panic buying and record-high insurance and shipping costs for oil transport in the Persian Gulf region.7 Traders drove prices up rapidly on worst-case scenarios. At the same time, refinery constraints and seasonal factors added pressure. U.S. refineries entered spring maintenance just as crude supply tightened, limiting gasoline production flexibility. Summer-blend fuel requirements, which help reduce emissions but are costlier to produce, and typical spring driving demand created an additional seasonal uptick in gas prices. As a result, refiners experienced a windfall: refining margins, known as crack spreads, for diesel soared to roughly $66 per barrel on the U.S. Gulf Coast in March, near record levels seen during the 2022 Russia-Ukraine shock caused by the start of the Ukraine war. This indicates that refining capacity was stretched, especially for diesel fuel, contributing to higher prices at the pump. Overall, the confluence of war-driven supply shortages, OPEC export cuts, and refining bottlenecks have sent fuel costs sharply higher in the short run.

How Higher Oil and Fuel Prices Are Affecting Inflation

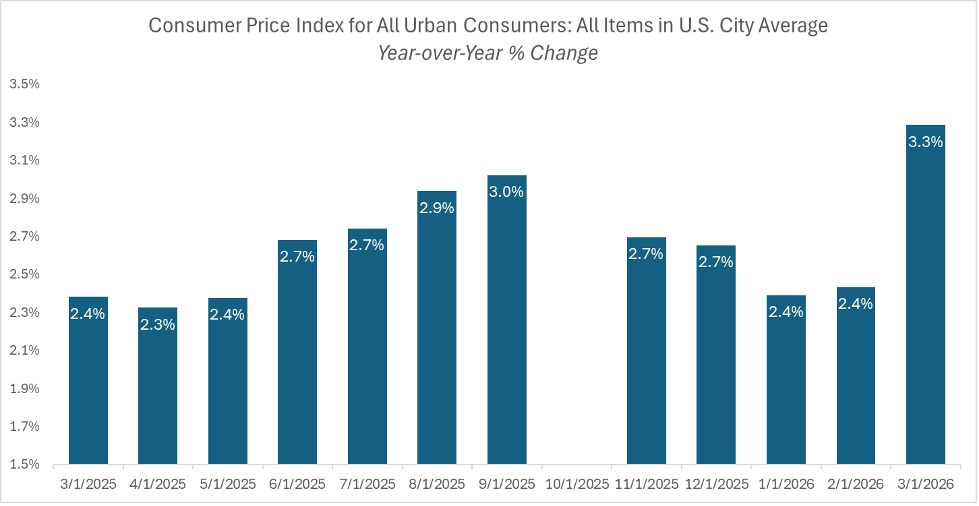

Fuel prices have an outsized impact on headline inflation because gasoline, diesel, and other energy items are directly captured within consumer price indices. The Consumer Price Index (CPI) rose 0.9% in March alone, three times the prior month’s increase, bringing headline CPI to 3.3% year-over-year (up from 2.4% in February).

Source: U.S. Bureau of Labor Statistics, JE Dunn Construction

Energy’s Outsized Impact

This jump was, as you would imagine after reading thus far, driven largely by energy: the CPI energy index jumped 10.9% in March– a record-setting surge.8 In fact, gasoline accounted for nearly three-quarters of March’s total inflation increase. Airfare costs rose as well, given the spike in jet fuel prices, and consumers faced higher costs for goods delivery and groceries as expensive diesel fuel filtered through supply chains.

Core Inflation Has Held Steady — For Now

Over in the “good news for now” column, core inflation (which excludes food and energy) showed a relatively stable reading so far. Core CPI was up 2.6% year-over-year in March, barely changed from February, meaning that the energy price shock didn’t immediately flow-through to other prices. In other words, outside of the energy-driven price hikes, broader inflation pressures have not (yet) accelerated dramatically and the fuel price shock’s effect on the costs of services has been limited.

Why Diesel Is the Indicator to Watch

However, those second-order impacts are on their way if high fuel costs persist. Diesel is particularly worth watching since nearly everything in the economy is transported by truck, rail, or ship, so steep diesel increases (40%+ since February) will likely translate into rising freight costs and ultimately higher prices for consumer goods in the coming months. Analysts note that the full effect of March’s diesel spike “has yet to be felt” and will flow through to the economy over the next few months as companies adjust their prices to cover higher shipping and production expenses.9 Similarly, agricultural products and construction materials will become more expensive due to higher fuel and fertilizer costs, affecting food prices and goods like plastics and asphalt. Any increase in fuel surcharges, delivery costs, and utility bills can feed into the core inflation rate indirectly over time, even though energy itself is excluded from core measures.

How Consumer Inflation Expectations Are Shifting

Inflation expectations have also ticked up in the wake of expensive fuel. American consumers tend to notice gasoline price changes immediately, and this can influence their perception of overall inflation. In April, one-year ahead consumer inflation expectations jumped to about 4.8% — the highest in over six months — from around 3.8% in March.10 Short-term inflation sentiment hasn’t been this high since mid-2025, reflecting the psychological impact of $4+ gas and headlines about oil prices. So far, longer-term expectations remain better anchored, staying near the Federal Reserve’s (Fed’s) 2% target on the five-year outlook. That means that while the current fuel shock is affecting how people feel about inflation in the near term, they don’t yet anticipate a permanent inflationary spiral (good news). That distinction is critical for policymakers, because well-anchored long-term expectations give the Fed more leeway to look through temporary price jumps.

The Federal Reserve’s Decision on Interest Rates

The Fed is closely watching fuel-driven inflation but is trying not to overreact to short-term energy volatility. At its late-March policy meeting, the Fed’s rate-setting committee chose to hold interest rates steady, despite the jump in headline inflation, citing uncertainty about the economic impact of the Middle East conflict. 11 Chairman Jerome Powell emphasized that energy price spikes will “push up overall inflation in the near term, but it is too soon to know the scope and duration of these effects.” Roughly translated, this means they will not immediately tighten monetary policy simply because gasoline is more expensive this month. Historically, central bankers often prefer to “look through” transitory energy shocks — focusing on core inflation as the best indicator of where prices are headed — as long as longer-term inflation expectations remain anchored. From the Fed’s viewpoint, a sudden jump in oil or gas prices is problematic for consumers but does not always require a policy response if it doesn’t fundamentally alter the broader inflation trajectory.

The Risk of “Non-Transitory” Inflation

However, the Fed is also keenly aware that a persistent fuel price shock could alter the inflation landscape. Officials have made clear that they will respond if energy-driven inflation shows signs of feeding into wages, core prices, or inflation psychology. For example, Fed Governor Christopher Waller noted that the recent oil surge changed his outlook: he had initially considered supporting a rate cut this year, but “prolonged elevated oil prices” could have a “non-transitory” impact on inflation, causing him to back away from easing for now (https://mariemontcapital.com/fomc-march-2026-treasury-yields-oil-shock/). Policymakers are again balancing two risks: tightening too little and allowing an energy shock to reset inflation higher, versus tightening too much in response to what may prove a temporary spike. So far, the consensus on the Federal Open Market Committee (FOMC) has been to hold rates steady and monitor incoming data.

Is This 1970s Stagflation? Why 2026 Is Different

It is worth noting that the current situation differs from the 1970s oil shocks, a comparison sometimes raised whenever fuel prices spike. While today’s supply disruption is severe, the U.S. economy is more energy-efficient and far less dependent on imported oil than it was decades ago. The nation is now a net energy producer, which provides some cushion– higher oil prices, while painful for consumers, also stimulate domestic drilling and energy investment, offsetting some economic damage. Moreover, unemployment remains low (4.3% in March) and core inflation near 2.5%- not what we saw with 1970s-style stagflation when double-digit inflation (14.6%) coincided with high joblessness (7%).

How the Length of Disruption can Impact Inflation

This volatility that we’re seeing can cause sharp, short-term swings in inflation, but the medium-term policy impact depends on duration. If the conflict in Iran is resolved or the oil supply disruption is cleared relatively soon, fuel prices could stabilize or even recede, allowing headline inflation to ease again in the coming quarter. The Fed’s stance is that a short-lived supply shock will largely wash out of inflation measures within months. Research by the Federal Reserve Bank of Dallas finds that a brief disruption, on the order of one fiscal quarter, would cause a significant temporary price level jump but leave inflation only about 0.3–0.4 percentage points higher by year-end as fuel markets normalize.

Of course, that math changes quickly if the disruption is extended. If oil prices were to stay in triple-digit territory for multiple quarters, the cumulative effect on prices could become more pronounced with scenario analysis suggesting that a nine-month Hormuz shutdown could send oil toward $150–$170 per barrel and boost U.S. inflation by nearly 2 percentage points by the end of the year.12 While this is a worst-case scenario, it underscores the tail risk of re-acceleration in inflation if the energy shock were to persist or worsen. In such a prolonged shock, households and businesses will have baked higher fuel costs into wages, contracts, and price-setting, creating a more entrenched inflation that the Fed would find harder to ignore.