As investors look ahead to 2026, there is growing confidence that real estate should continue in a positive direction toward a long-term cyclical recovery. As an investor, JE Dunn Capital Partners is constantly studying economic indicators and market-specific factors to help predict timing, pricing, and risk for projects. This year, we expect many investors to come off the sidelines after two consecutive years of high interest rates and economic uncertainty. Even though JE Dunn is cautiously optimistic for 2026, there is an array of ever-evolving factors that could impact outcomes.

Debt became substantially more available in 2025 than the previous two years, and we see that trend continuing through 2026. Furthermore, debt cost reduced by as much as 40% from 2023. However, major institutional equity largely remained on the sidelines in 2025 for new developments such as high-rise multifamily in urban markets. At the same time, a historic wave of multifamily supply depressed rents while construction costs continued to escalate. These factors crushed financial pro formas, stalling a large portion of new deals nationwide.

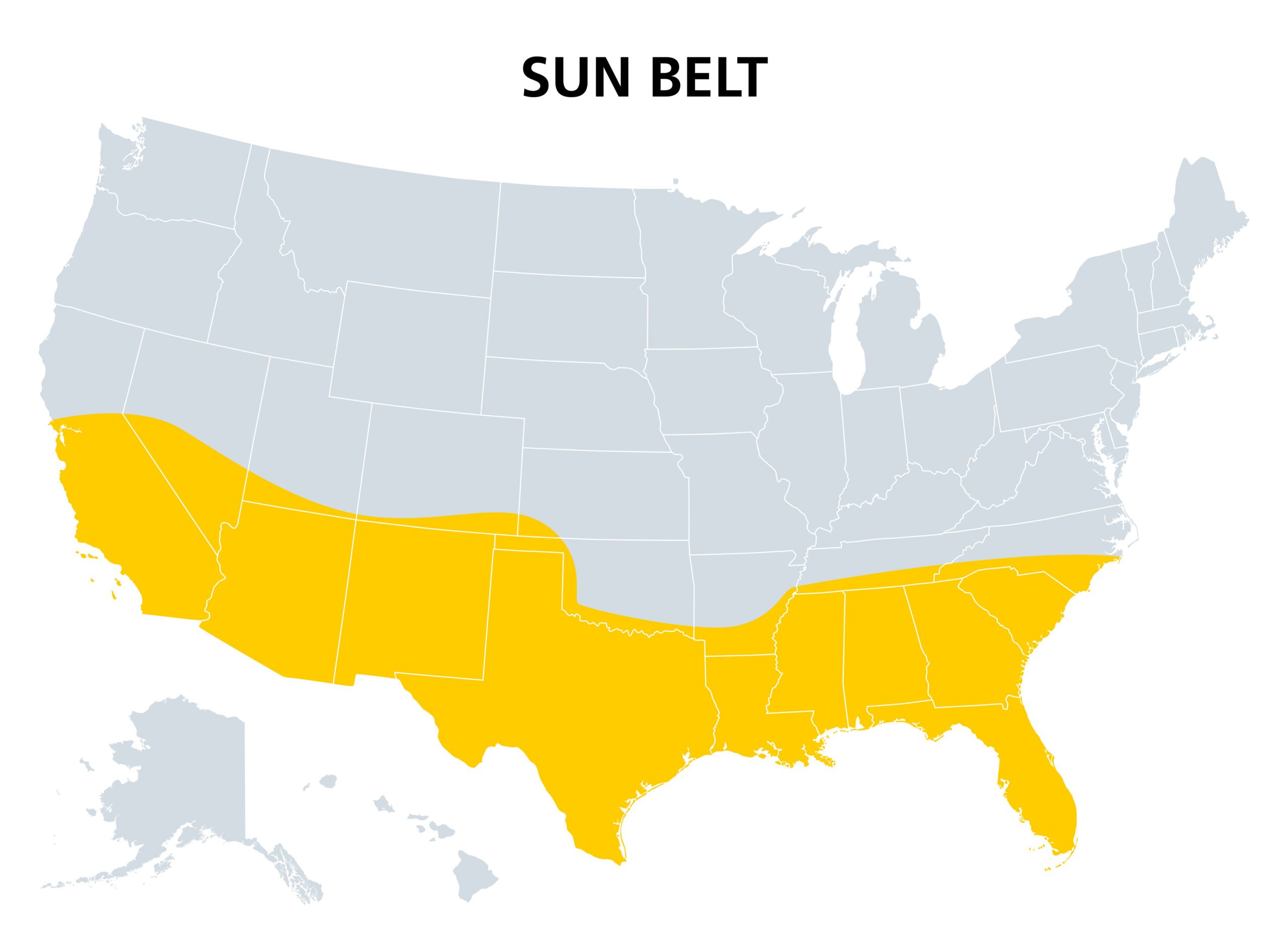

We believe that strong growth markets in the sunbelt, such as Dallas, Austin, Tampa, and Charlotte, will continue to absorb the multifamily supply and create a new opportunity for favorable rent increases one to two years ahead. Given the slower, non-data center construction volumes, there is optimism that construction costs in urban markets will minimally escalate. If the above factors hold true, it will create significant opportunity for developers to find a new path to financial feasibility. This dynamic shift should create a new wave of general commercial construction starting in late 2026 and carrying into 2027 and beyond.

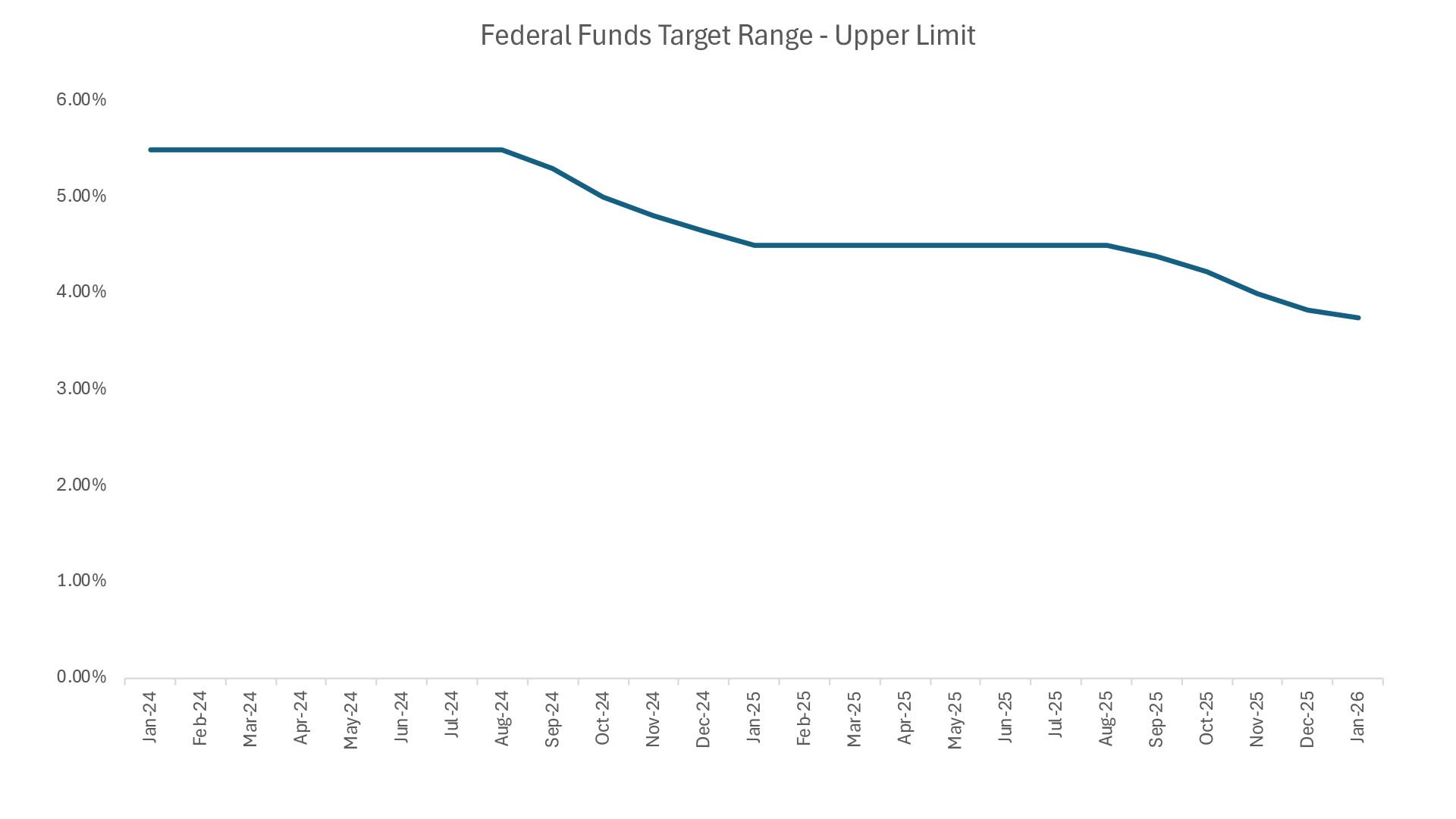

Interest rates are another key factor in the commercial real estate markets. Rates hovered around 4.5% in 2025 until the Fed cut rates three consecutive times, bringing the range to 3.5 to 3.75%1. At the Fed’s first 2026 meeting, they decided to halt rate reductions as expected.

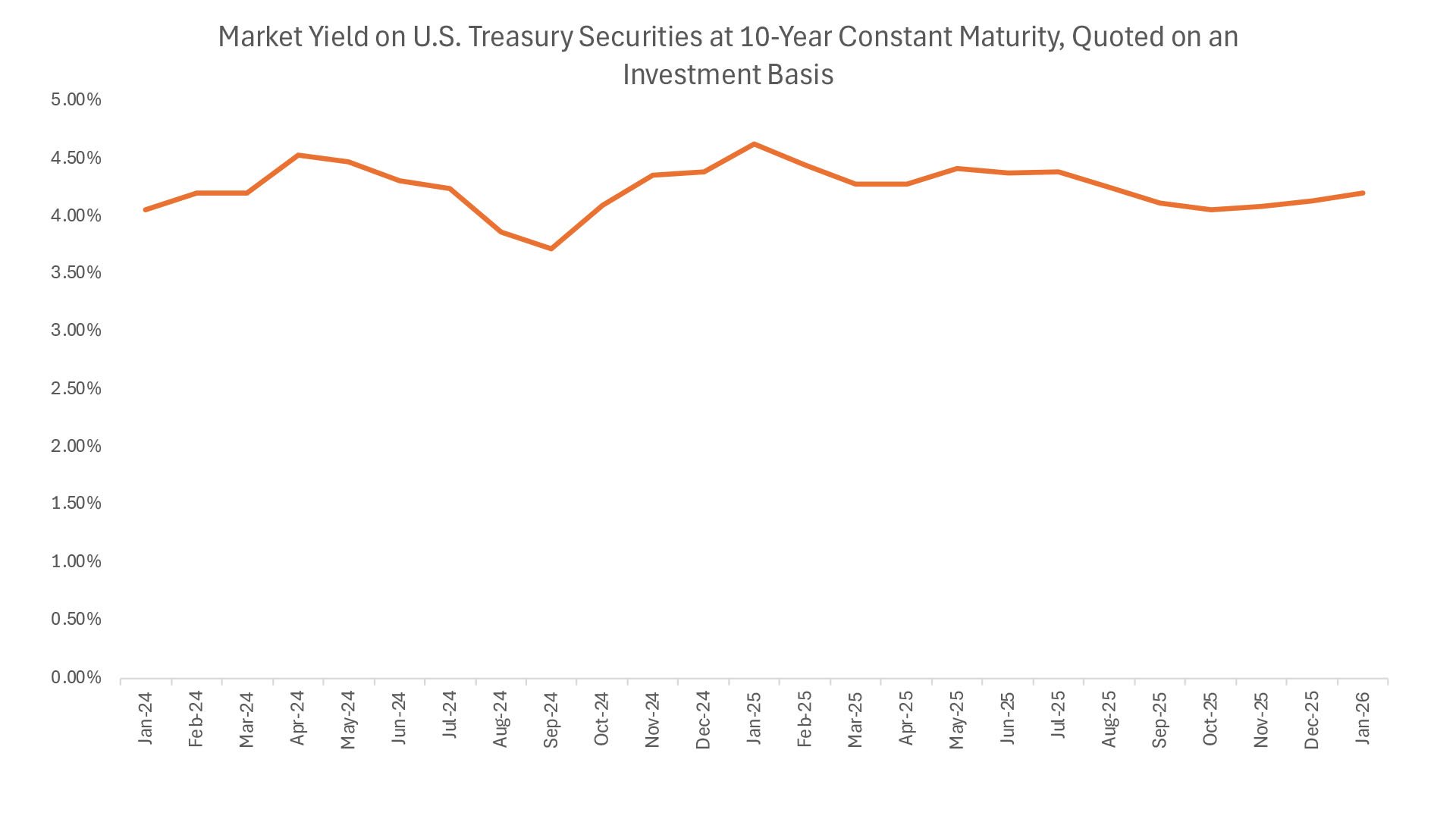

Meanwhile, throughout this rate-cutting period, the 10-year Treasury, which is a key metric in real estate finance, has stubbornly hovered at or slightly above 4% due to sticky inflation, trade tensions, and U.S. budget deficits and increased issuance of treasuries2. Based on our research, we anticipate a couple more rate cuts this year. However, even if the 10-year remains stubborn through 2026, the growth of AI-infrastructure, housing supply shortages, and e-commerce/logistics should continue to buoy the real estate market into ongoing recovery.

For the very near term, it will likely continue to be a tale of two markets between data centers (and all AI related infrastructure) and everything else. Demand for data centers and related AI infrastructure is rewriting the definition of “core” real estate, driving new capital and innovation into this sector, while traditional asset types such as office, retail, and hospitality experience a slower recalibration.

Another critical theme shaping commercial real estate is the widening gap between asset classes and geographic regions. While data center demand remains robust, office, in particular, continues to face headwinds, even for top-tier, amenity-rich buildings in vibrant submarkets that continue to attract tenants, due to elevated vacancy and financial strain that have slowed the overall pace of growth. This divide is prompting many owners to reevaluate their long-term strategies, weighing whether to reinvest, repurpose, or exit challenged assets.

At the same time, investors are increasingly attentive to demographic and migration trends. Population growth in sunbelt metros continues to outperform coastal gateway cities, fueling demand not only for multifamily but also for industrial, medical, education, and neighborhood retail. These markets benefit from business-friendly environments, favorable tax structures, and ongoing corporate relocations — conditions that are likely to persist through the decade. As these metros mature, we expect to see greater diversification of investment opportunities, including mixed-use districts, adaptive reuse developments, and infrastructure-oriented projects that support growing populations.

Technology will also continue to influence both development feasibility and operational performance. Advancements in AI-enabled design, estimating, and scheduling are reducing uncertainty in preconstruction and helping owners achieve clarity earlier in the development cycle. On the operations side, smart-building systems are improving energy efficiency and tenant experience — attributes increasingly demanded by institutional capital. As regulatory pressures around sustainability intensify, assets that incorporate energy-efficient systems, electrification strategies, and resilient design features will be better positioned for long-term competitiveness.

Overall, while pockets of the market remain challenged, the combination of easing financial conditions, structural demographic strengths, technological adoption, and a stabilizing cost environment positions 2026 as a pivotal year. If current trends hold, the industry appears poised to transition from a defensive posture toward a new cycle of thoughtful, strategically aligned growth.