There has been a flurry of headlines warning of a potential recession, but before diving in, it’s worth pushing back against the popular rule of thumb that defines a recession as two consecutive quarters of negative GDP growth. In reality, the National Bureau of Economic Research, the official authority on U.S. recessions, uses a broader definition: “a significant decline in economic activity that is spread across the economy and lasts more than a few months.”1

While back-to-back negative GDP quarters often coincide with recessions, they’re not always a reliable rule. Recessions can vary dramatically in length and can even be shorter than two quarters, such as the 2020 recession that lasted less than one quarter, and some recessions have occurred even as GDP grew. GDP is a lagging, often-revised metric that isn’t great for real-time analysis.

Recession talk is growing louder due to some soft economic data and the Atlanta Fed’s GDPNow model, which has shown significant negative GDP growth in Q1 2025 for the past several weeks.2 But GDPNow is not a forecast in the traditional sense — it’s a real-time estimate based on data received so far. As more data comes in, the estimate will evolve. The Atlanta Fed describes it as a “running estimate…based on available economic data for the current measured quarter.”

Still, the data isn’t encouraging. For the GDP figure to turn positive, the remaining reports will need to have stronger results. Another red flag: consumer confidence. Consumer spending — critical to the U.S. economy — has kept a recession at bay despite high interest rates. But earlier this quarter, confidence fell by the largest amount in nearly four years, despite relatively positive economic news not long ago. The biggest driver of that drop? Likely, uncertainty.

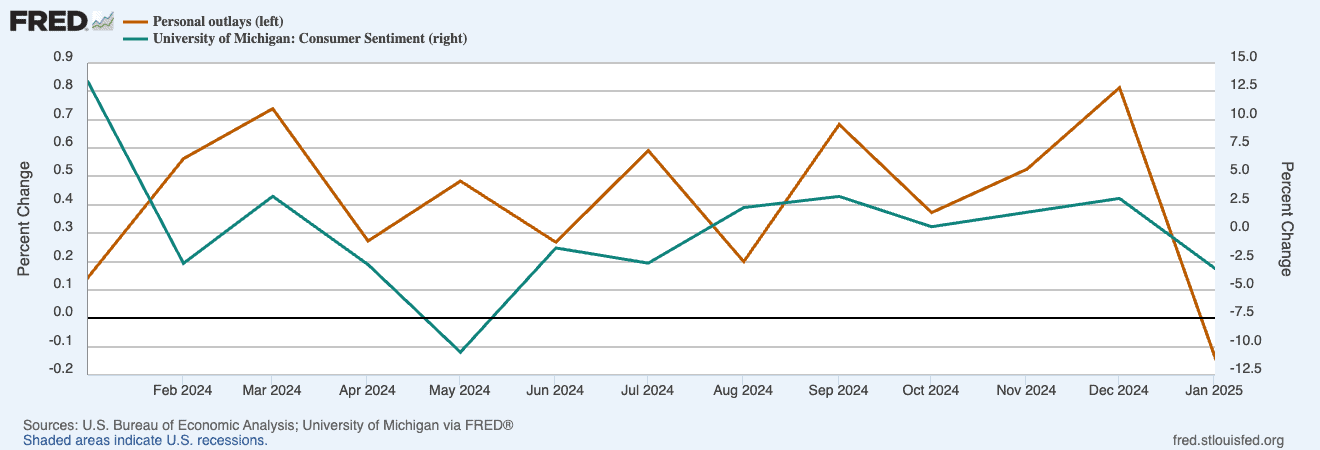

Here’s a look at how sentiment and spending move:

Consumer sentiment has been low before, but it hadn’t translated to weaker spending — until the January data showed a decline. A shift in behavior could be tied to labor market signals. Mass layoffs are making headlines, and the four-week moving average of initial jobless claims — a proxy for layoffs — has risen notably since early February.

These trends do raise the risk of a near-term recession. In March, Goldman Sachs increased their 12-month recession odds from 15% to 20%, Yardeni Research from 20% to 35%, and J.P. Morgan now sees a 40% chance.3 Former Treasury Secretary Larry Summers recently said there’s a “real possibility” of recession.4

While risks are rising, it’s from a relatively low base. The economy performed well through late 2024, and the Fed seemed to be achieving a rare “soft landing.” More warning signs may emerge, but for now, the economy is more likely the headed toward a slowdown rather than a full-blown recession.